Future Outlook : The numbers speak for themselves

Global

We are heading into a critical zone as far as world markets are concerned with mega events about to unfold: (i) The US presidential elections and its aftermath, (ii) unabated Chinese muscle flexing and the subsequent US, neighbouring countries and World response, (iii)continuing global spread of COVID-19 and its economic and social impact. Applying lessons learnt from the global financial crisis, global central bankers and governments have loosened their purse strings with impressive speed to help ease financial conditions and avert drying up of financial liquidity. With all the good this has done; it has given rise to some risks including a parting of ways between Wall Street and Main Street and unsustainable levels of debt for some borrowers that may test the global banking system in times to come.

From an anticipated 3.3% growth prediction in January to -3% in April, the IMF has, in June, predicted a -4.9% growth for the global economy for 2020 (source). Global economies have recovered swiftly from the massive collapse they suffered in the first half of 2020 as countries opened up for business, limping back to whatever the new normal holds for us. Except China, where the virus is from, almost all other G-20 countries suffered a recession (source). South Korea and Taiwan managed the virus pretty well while the USA, Brazil and India have been worst affected.

Local

India paints a mixed picture. After posting a 4.2% GDP growth in 2019, India is expected to de-grow by over 10% in 2020 and then grow back by nearly 10% in 2021 resulting in a total loss of at least 2 years’ worth of productivity (source). The COVID-19 impact continues to challenge the healthcare system with over 90,000 cases and nearly 1000 deaths per day. The saving grace is the lower mortality rate and robust recovery rate despite opening up large swathes of the economy. Incoming data points including power consumption, mobility indicators, vehicle registrations, etc. are pointing to a gradual recovery. Unlock4.0 has allowed a large part of the economy to start controlled functioning including malls, gyms, and restaurants. Unlock 5.0 has come with some measures for opening up of schools, universities, cinema halls, swimming pools, entertainment parks, etc. International flights are still out of bounds save for the air bubble arrangements with other countries. Rural markets continue their growth trajectory with a good monsoon season behind us, and continued front loaded government support. Credit growth and sticky inflation remain the larger concerns for now even as we wait for the true level and impact of non-performing assets in the economy and the resultant challenge to bank balance sheets.

Startup Ecosystem

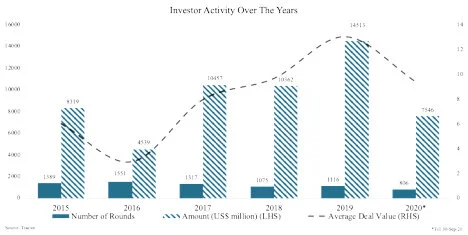

As things start normalizing in India, or as close as we can get to it, the outlook for the startup ecosystem is optimistic. The second quarter has seen a 40% uptick in the number of deals (from 247 to 345) - the most we have witnessed in a quarter recently, coupled with an 88% increase in capital invested (from US$ 1.68 billion to US$ 3.17 billion), resulting in a 12% increase in the average deal value (from US$ 8 million to US$ 9.19 million). As we journey along the road to recovery, it might do us well to recall the second quarter of FY20. On a Y-o-Y basis, 2Q21 has shown a modest uptick of 2% in the number of deals (from 336 to 345), while capital invested has shown a drop of 31% (from US$ 5.38 billion to US$ 3.17 billion), resulting in a 32% fall in average deal size (from US$ 13.61 million to US$ 9.19 million). The numbers speak for themselves - investors are flocking to this class of alternative assets and backing companies earlier in their lifecycle. As we venture into the third quarter, the most active quarter for venture deals, past trends are likely to prevail and better numbers are likely to be clocked.