The World As We See It

Global

Investors have a lot on their hands today. We would say that investors have never faced such uncertainty in the past. Global financial crisis - bam. Done. It happened swiftly and left us managing the aftermath. The Dotcom crisis - a flash in the pan when we look back at it now. It wrote new rules for e-commerce and internet applications. Today’s scenario includes a slew of risk variables to consider: QE tapering and rising rates, slowing GDP growth, trade disruptions, massive global debt positions, geopolitical flashpoints (Ukraine, Taiwan, the Middle East), looming COVID resurgence (possibly a deadlier variant), fragile markets in some asset classes (crypto, yes, trillions of dollars invested here so it remains relevant), high-frequency trading, illiquid ETFs, etc. If this were it, the uncertainty would be limited since we would clearly be in the throes of a recession and a bear market. Things are not that simple because we have, on the proverbial other hand, fiscal stimulus possibilities, easy financial conditions that continue to prevail, several markets near their all-time highs, equities at this time are not the most expensive, cash positions are accessible and waiting to be deployed (dry powder with VC, PE investors, household savings), the belief that higher valuations (PE and other multiples) are here to stay, etc.

The World Bank, in its latest report on Global Economic Prospects, January 2023, forecasts a sharp, broadbased, and long-lasting slowdown across virtually all regions of the world. They forecast global growth to decline to 1.7% in 2023 from the 3.0% expected just six months ago.

The ripple effects of Russia’s invasion of Ukraine, US monetary tightening, and an economic slowdown in China may weigh on global economies this year. Growth projections have been downgraded for almost all advanced economies. The US growth forecast is at a mere 1%. In the Euro Area, growth is projected to come in at 0.2% after conjecture about contraction. China’s economy is forecasted to grow at 4.0%, and Emerging Market growth is forecast at 2.9% in 2023.

Asset prices continue to be in broad, synchronous decline, investment growth has meaningfully weakened, and housing markets have weakened across many countries.

Looking into 2023 much depends on inflation, interest rates, and the direction of the US dollar. In an environment where all are seeking what will or can go wrong next, it may be worthwhile to ask a slightly different question: what can go right?

India

As the global economy stares at a possible recession, India may not be entirely immune completely from the spillover effects. That said, India’s economy displayed brief bursts of strength in the third quarter of 2022, resisting the general trend and narrowly beating forecasts for growth of 6.3% Y-o-Y. For 2023, the RBI foresees a 6.8% GDP growth in India. The RBI estimated 6.8% GDP growth for FY23 in India.

The economy is in relatively good shape, with a strong GDP and declining inflation. India's CPI inflation fell below the RBI's target in December 2022 to a one-year low of 5.72%. This drop in inflation raised expectations of a more modest increase in the repo rate. In December 2022, the RBI responded by raising the repo rate by 35 basis points. RBI this year increased the policy repo rate by 225 basis points so far taking it to 6.25%. Core inflation, though, continues to stay elevated and sticky.

Even as the Indian rupee hovers close to its lifetime low this quarter, depreciating 10.4% since January 2022, making it one of Asia's weaker currencies, it is expected to trade in a tight range in 2023. The good news is that corporate debt has dropped from 62% of GDP in 2016 to 47% today, giving corporate India confidence to expand its capacity. As a share of GDP, central government capital expenditure is now at a record high of 2.9%, up from a low of considerably below 2% throughout the course of the previous five years. Aggregate capacity utilisation was 77.6% and remained above the long-term average of 73.3%.

While India’s reserves had touched an all-time high of US$632.9 billion in February 2022, they have since slid to $US561.5 billion as a result of the RBI’s interventions to defend the weakening rupee from an escalating US dollar. Reserves fell to its lowest point in October 2022, at US$468.8 billion. The good news is that India's external standing has dramatically improved. The highest-ever annual FDI inflow to India was US$83.6 billion in FY21–22, and remittance flows climbed by 12% Y-o-Y from US$89.4 billion to US$100 billion.

India continues to demonstrate resilience, with domestic demand remaining broad-based, improving sentiment, better job prospects for its young population, and stronger balance sheets supporting the ongoing capex cycle. India will play a vital role in the global economy in the following decades as it outperforms all other significant middle-income nations.

Early Stage Ecosystem

Investments in the early-stage ecosystem remained largely stable during the quarter, with no significant changes. This quarter saw a 15% rise in capital invested, from US$4.4 billion to US$5.1 billion, while the number of deals saw a 6% dip from the previous quarter from 535 to 503. The average deal size saw a 22% jump, reaching 5,116 from 4,442 in the last quarter.

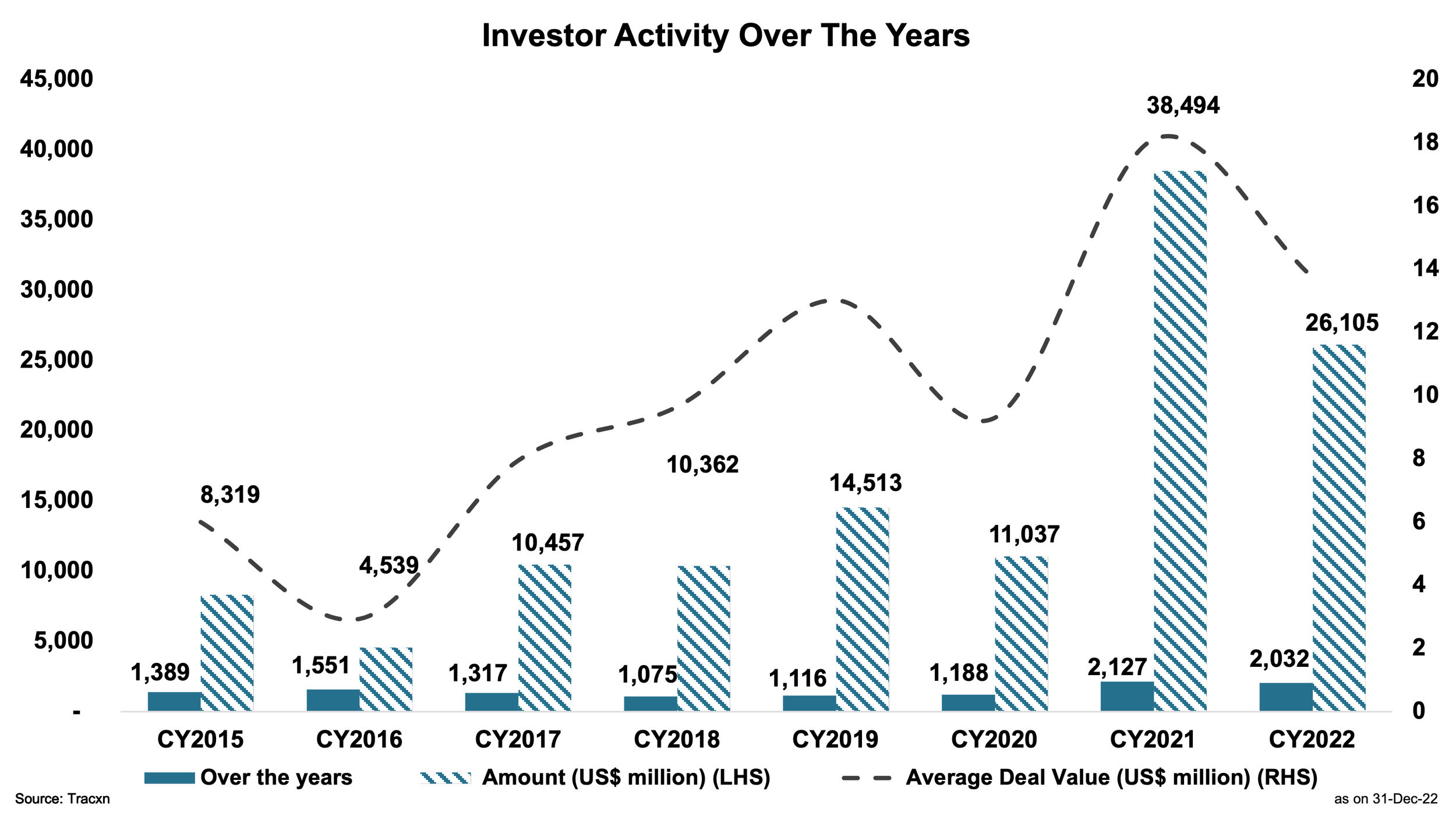

The year 2022 was all about the survival of the fittest. It ended on a somewhat optimistic note for the earlystage companies, while most growth and late-stage companies were seen navigating icy roads. Overall investments fell from a high of $38 billion in 2021 to US$26 billion in 2022, a drop of 35%. While the average deal value dropped by 29% from US$18.1 million to US$12.8 million, the number of deal rounds saw only a slight dip of 4% from 2127 to 2032. The ongoing liquidity squeeze has forced startups to build more precise and sustainable growth paths. They were compelled to reassess their plans to weather the storm, emphasising cash management and enhancing unit economics. Investors have now started demanding a route to profitability as they scrutinise valuations, which is excellent for the overall ecosystem in the long run.

India, thus, witnessed a lesser number of unicorns as well as fewer anecdotes of barrelling valuations, while most unicorns were seen chasing profitability. The investment raised by late-stage companies was down by 40% from that in 2021, falling from US$35.5 billion to US$21.3 billion in 2022. It should be noted that early-stage companies, in contrast, were seen to be better positioned to stay in the game. In 2022, the total investments in early-stage companies increased by 11% compared to the previous year from US$4.3 billion to US$4.8 billion. The average deal value saw a 32% jump compared to 2021, from US$2.2 million to US$2.94 million, despite a 16% decline in the deal count in 2022 compared to 2021, from 1946 to 1636. Sector-wise, fintech continued to lead, followed by e-commerce, SaaS, healthtech, and edtech.

India’s startup environment has evolved dramatically over the years. It moved steadily until 2019 and has evidenced a shift since then. The year of the pandemic, 2020 saw the ecosystem advance from basic survival to sustainability as an outcome of a more technologically advanced country. 2021 was an outlier; the capital inflows and the number of unicorns peaked. 2022 put the Indian entrepreneurial ecosystem to the test, and amid all the gloom, the ecosystem underwent a lot of forced corrections.

Yet the nation’s ambition to become a world-leading startup ecosystem has remained unaltered, backed by robust domestic demand. In less than a decade, we managed to rank ourselves third worldwide and have emerged as a bright spot for global investors looking to deploy money.

While it is tricky to predict the sentiments of 2023, one thing that will not change is your Fund’s strategy of backing repeat founders, seasoned teams, innovative business models, and known markets.